Civil Discourse

2011

-

I. Introduction

In some sense economics is fundamentally about wealth; how it is created, how it is used, what privileges and responsibilities go along with having it, how it changes over time, etc. So let's start with what it is. I suppose in its simplest form we are relatively more wealthy when we possess more of the assets that we value highly. Some of these have an extrinsic value (i.e. a value to others as well as to ourselves) so that we can use them as part of economic activities that we undertake. Some have only an intrinsic value to ourselves alone. That does not in any way diminish their worth. In many cases we value such assets so much that we are willing to exchange any number of other assets with extrinsic value in order to acquire, retain, or add value to them.

This definition of wealth is first and foremost a personal measure. I might consider myself to be an extremely wealthy person and someone else looking at me might consider me to be relatively poor. To the degree that most members of a given society share common values and desires, there may be a general consensus about who is wealthy and who is not, but that consensus is almost certainly not a unanimous opinion.

In western cultures we often reduce the notion of wealth to some personal cash equivalent even though at some level we know this is not the whole story. Other cultures have considered personal wealth to be irrelevant and group wealth to be of paramount concern. So the notion of wealth is both personal and culturally derived.

I think those of us who reside in western cultures might agree that giving each individual the opportunity to achieve wealth according to their own personal values would result in a wealthy society. I believe that's what most of us mean when we talk about having a "free society". When relatively more of us are wealthy, in whatever personal sense that has for each of us, then the society as a whole is also relatively more wealthy. We view the accumulation of aggregate wealth as the highest goal of our society and create governments, laws, and organizations which foster the growth of aggregate wealth.

But note that aggregate wealth can be distributed among the population in many different ways. You can have a smaller minority of persons who are extremely wealthy with a much larger group that is much less wealthy. Or you can have a large homogenous group who are only moderately wealthy. And of course there are middle grounds between those two extremes. What is the most desirable distribution? We'll see later in this paper why I think that answering this question is not as simple as we might initially believe, but is fundamental to shaping a society. We'll also talk about how this exact same notion of maximizing societal wealth can lead to dramatically different social and economic systems when fundamental societal values are different.

-

II. Model Concepts

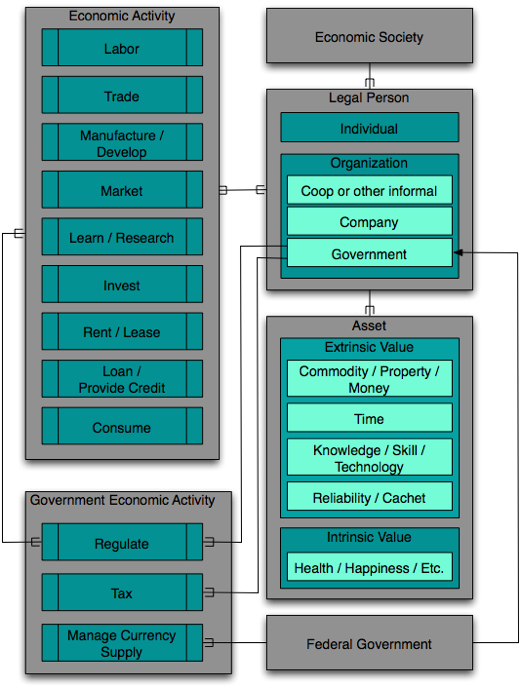

Comprehending sometimes esoteric economic concepts can a challenging task. I know that until I found a relatively simple way to group various concepts into simpler groups I had a very difficult time understanding more complex economic ideas. My simplified diagram of economic concepts is shown above. This is entirely of my own devising and probably isn't comprehensive, but seems to work for me.

For those who aren't used to looking at diagrams like this it's probably worth saying a bit about the notation used. The gray boxes represent types of entities or concepts. Any box of a different color within a larger box represents a subtype of that larger box. So, for example, LABOR is a type of ECONOMIC ACTIVITY, an INTRINSIC VALUE is a type of ASSET, and CACHET is a type of EXTRINSIC VALUE. The lines that connect boxes represent relationships between concepts. The pitchfork end of a line indicates that there are potentially many of those entities involved in the relation. So for example the diagram could be read as saying that an ECONOMIC SOCIETY is composed of many LEGAL PERSONS. The line connecting ECONOMIC ACTIVITY and LEGAL PERSON could be read as saying that an ECONOMIC ENTITY engages in many ECONOMIC ACTIVITIES and an ECONOMIC ACTIVITY involves many ECONOMIC ENTITIES. The line connecting FEDERAL GOVERNMENT to GOVERNMENT represents the same subtype relationship that embedding a box within a larger one does. So I could have just put the FEDERAL GOVERNMENT box within the GOVERNMENT box. But for this model the federal government play such a central role that it was better to make the box stand alone.

What this diagram suggests is that we can talk about an economic society as being composed of legal persons (either humans or organizations) which hold assets of different sorts and undertake any of various economic activities within an environment governed by some set of regulations. Those activities, generally speaking, transform one set of assets into a a second set of assets. If all goes well, the second set has more value than the first set although there is never a guarantee that that is the case. When that does occur, the legal person has increased his or her or its wealth. As we'll see later, the best economic activities increase the wealth of all parties involved.

Most readers will have an innate sense about what the words in that last paragraph mean, but undoubtedly they will mean slightly different things to you than they did to me when I wrote them. So in the paragraphs that follow I'm going to expand on each of the concepts in the diagram to help explain what I was thinking when I created it. There is no particular reason to accept my definitions other than to use them to understand points that I make later. I wish there to be as little confusion as possible about what I have to say.

II.A. Economic Societies

An economic society, for purposes of this discussion, is just a collection of legal persons that can be either individuals or organizations. This concept of legal person is more or less consistent with the IRS's notion of a taxpayer although as you'll see in a bit, what I have in mind is more inclusive than that.

When most people think of a "society", they probably think primarily about their own country. But I mean the term to be broader than that. In the sense that I mean the word, we all live in many different societies simultaneously. In the United States we may have different societies at local, regional, county, and state levels. In addition we exist in an international society. All of these are what we might think of as economic societies; that is, they exist for the purpose of conducting economic activities. There are also religious societies, social societies, sports societies, and many others. For purposes of this paper I want to restrict my discussion to economic societies with the caveat that some forms of economic society may not be purely economic in nature. For example, in many parts of the world religious and economic societies are either very closely connected or identical. Understanding this can aid in understanding these societies better.

Societies have distinct cultures that ultimately define the values held by its members. These values can influence the type and nature of the economic activities which their members undertake. They can also influence the types of assets that they hold and more importantly the value that they place on different types of assets. Economic activities are all about increasing asset value so therefore culture plays a big role in economics.

II.B. Legal Person

I view virtually every human in a society as a legal person, whether or not they actually own any physical assets or pay taxes. This includes children, the very elderly, unemployed vagrants, everybody. As we'll see in a bit, they clearly carry out actions with economic consequences. Any discussion about how an economy functions would be incomplete if it didn't include all of them.

Organizations are also legal persons. They can own property and undertake economic activity in virtually the same manner as individual humans can. I would also include non-profit organizations in my idea of what an economic society is. They too carry out economic activities. And as I suggested above, governments are also legal persons, although of a very special sort. The Federal government in the U.S. or any foreign government that prints and controls its own money have even more specialized roles that will be discussed in great length later. The box labeled "Federal Government" represents these.

From now on, when the term person is used, it will refer to a legal person in this sense, rather than to some individual human being.

II.C. Federal Government

Federal governments are the U.S. government or any sovereign foreign government that issues and manages a currency that is not tied in value to any other currency or commodity. Previous to 1971 even the U.S. government would not have fit the last part of this definition because the dollar had a value that was fixed to a certain amount of gold. When President Nixon officially took the country off the gold standard the government gained some capabilities that were not immediately obvious and are still widely misunderstood today, not only by the average citizen, but also by government officials and even many professional economists.

Note that under the terms of the European Economic Union agreement, its members no longer control their own currencies. Their adoption of the Euro means that no single country can unilaterally decide to deficit spend in Euros. Each of these countries is now more like a U.S. state in the sense that they are users of the currency, but not originators of it. We'll see the significance of that later, but suffice it to say that I believe this accounts for many of the problems currently faced by Greece and other members of the EEU.

II.D. Assets

An asset is something which a person possesses and has control over. There are many possible ways that one might further categorize assets. For example, we could talk about tangible versus intangible assets. We could talk about capital vs non-capital assets. One of the more useful ways that I've found to enhance my own understanding is to differentiate between assets that have an extrinsic value and those that have an intrinsic value.

Assets can change form or character over time or as they are affected in some way by an economic activity of the sort described later. Assets can be such that they can be used once and are gone (e.g. money or time). They can be perpetual and used over and over again (e.g. knowledge). They may be self-renewing in some form or virtually inexhaustible (e.g. solar energy). Assets may depreciate over time; age decreases their value (e.g. buildings, technology, health). Assets may appreciate over time as well (.e.g. property that becomes surrounded by other development, stocks). Many of the economic activities that will be discussed try to take advantage of asset changes over time to create wealth.

Value

When I use the word value I mean the relative desirability of an asset to its owner at some point in time. Assets themselves do not have a unique or enduring value. Rather we can talk about the value of an asset to a particular person or entity at a particular time. An asset's value to a particular person at a particular time can be measured in terms of what other assets that person would be willing to exchange to get it. Each person has its own set of values that determine what sorts of economic activities it will enter into. I will have more to say about this after some additional concepts have been defined.

Extrinsic versus Intrinsic Value

An asset that has an "extrinsic value" is one that can have value to some person other than the one that currently possesses it. Therefore they can be acquired and/or used in various economic activities. In the general parlance of economists we might say that these can be monetized, that is, we can exchange them with the assets of others. Assets with "intrinsic" value are fundamentally developed and/or acquired by and for the benefit of the single person that possesses it. Let's see if an illustration can make this difference more meaningful.

We all want to be healthy. To do this we may go out and acquire health care or knowledge about how to care for ourselves. We may invest time in exercise to keep ourselves fit. And of course we buy and consume food in order to stay healthy. Each of these activities is a form of economic transaction. But once we have acquired good health, it is not something that typically has an extrinsic value to to others. We have to be a bit careful here because clearly people like professional athletes exchange not only their skill, but in some sense their health as well, for monetary compensation. And I know several former co-workers who might tell you that they exchange some of their happiness for monetary compensation.

So take this categorization with a small grain of salt and recognize that although we'll find the distinction to be a useful one, it is not meant to provide a rigid boundary. My primary reason for talking about assets is that they are the things exchanged by economic activities.

Examples of Extrinsically-Valued Assets (EVA)

The prototypical EVA is certainly money. We very often state the value of other EVAs in terms of some monetary equivalent. It is easier to get wound around the axle when thinking about money than with any other economic concept that I encountered in my research. There are several different schools of economics that each see things in their own way. Although I'll make an argument for why you should accept the view that I have come to believe is correct, there are many smart people who see things differently, so you'll need to make up your own mind about whether I've been convincing.

Physical property and commodities of various sorts are closely related EVAs. They could be property in the sense of real-estate or property in the sense of things that you can touch. These are very tangible sorts of EVAs.

Time is a fundamental EVA that each individual possesses. It has extrinsic value because we can each trade some of our time for other compensation. The value of our time to others varies according to how much of what they value they can get by using it in some fashion. If someone wants to move furniture or design a nuclear reactor they probably won't value my time very highly. If, on the other hand, they need a computer program written, then the value of my time to them would likely be quite a bit higher. The value of time to the person who has it is another matter altogether. That can vary quite significantly depending on their own current situation. A person who is otherwise fairly wealthy may prefer to use their time to increase some intrinsically-valued asset rather than do hard menial labor. But for a person in desperate need of a meal, the value of their time may be quite reduced relative to the value they would place on getting food.

The third general category of EVA shown in Figure 1 is labeled "Knowledge / Skill / Technology". This is a rather interesting form of asset. It can be acquired from others or transferred to others. It can be bundled with Time and used in economic activities such as teaching, consulting, or skilled labor. It can exist in the form of patents that can be used or transferred. We'll talk more about this sort of asset as we discuss various economic activities.

The last category of EVA in Figure 1 is labeled "Reliability / Cachet". These are intended as examples of course and do not nearly cover the scope of what is intended here. These assets are intangible assets in the sense that you cannot directly touch them or give them to someone else. But they have a definite extrinsic value. Companies can and do charge more for products that have these properties.

Examples of Intrinsically-Valued Assets (IVA)

IVAs are typically intangible and usually can't be directly monetized. I think of these as items that we value personally. We want to be happy, healthy, wise, respected, loved, content, beautiful/handsome, secure in our religious convictions, have self-esteem, etc. The reason that I added this asset category is that so many of us spend so much of our lives and fortunes (i.e. our other assets) striving to get them. Many people would say that ultimately some of these are the most important assets to possess.

II.E. Economic Activities

Generally speaking, persons engage in economic activity to increase their wealth. Each of the activities shown in Figure 1 is capable of generating wealth in a slightly different manner. Each carries with it the risk of decreasing wealth as well. Some types are innately more risky than others and within each type category there can be varying degrees of risk involved with different specific activities. I'll try to point out these risks as I describe each type of activity.

In general what all of these activities have in common is that there are assets that are used as input to the activity and other assets that are the result of the activity.

One measure of how beneficial an economic activity is in terms of creating wealth is its profit. That is usually thought of as the difference between the value of the outputs and the cost (value) of the inputs. Obviously the higher the profit of an activity, the more wealth it creates. Note that this crucially depends on the value of both the inputs and outputs. If all inputs are purchased or otherwise acquired for monetary consideration, as is often the case for manufacturing or other business activities, then the value of inputs is known with certainty. But the expected value of future outputs is often a guess at best and depends on the degree to which those assets will be desired in turn by others. Once the outputs have been actually sold to others, then the actual profit can be determined with complete accuracy.

In contrast, if the economic transaction is one of an individual selling their labor, then the value of the wage they'll receive (the output of the transaction from the individual's point of view) will be known in advance, but the (intrinsic) value of the use of their time may not be completely appreciated. It is also extremely difficult to put a currency value on the use of an intrinsically valued asset. In such cases it may not be possible to compute a precise profit value, but typically the person will still have some innate sense of the relative profit provided by the transaction.

In either of these cases the expected profit of a future activity may turn out to be in error. This will likely result in some revision of the terms of future transactions of a similar nature. I'll have more to say about this later.

The profit margin of an economic activity is the ratio between the profit and the value of the outputs. It is as precise or imprecise as the values of those two factors themselves.

The ratio between the value of the outputs of an economic activity and the cost of the labor used to create them represents the productivity of that labor. When we sell our time in the form of labor we typically also bundle our knowledge and skill with it. It is usually those additional assets that make us more productive and therefore make our time more valuable to the person who hired us.

The application of technology assets to an economic process can also improve the productivity of the labor used. We'll see later that for many sorts of economic activity the use of technology to improve productivity has become much more important to producing greater profits than the use of more skillful or knowledgeable labor.

Labor

Above I pointed out that the one asset each of us has is time. Labor is an activity where we exchange some of our time for compensation. This is perhaps most frequently some form of monetary compensation, but when we volunteer our time we exchange it for some form of IVA instead. Wealth is created for us when we value the asset we received more than we value the time itself. As I said somewhat tongue-in-cheek above, we may have to throw in a bit of happiness along with our time depending on what it is that we are asked to do with it. That is why we might take a job that pays less, but is less draining and perhaps even rewards us with additional IVAs.

Is there any risk associated with providing labor? The primary risk is not being compensated by the hiring entity for some reason. The risk is more substantial when laboring for another individual person or as part of a cooperative effort or for a small or new organization. But any labor can carry this risk.

There is also the risk that the profit of providing labor may not have been as large as anticipated. Perhaps providing the labor cost us more in terms of lost IVAs than we anticipated.

So it seems pretty obvious that we can increase our wealth by engaging in labor, but how does the person that hires us get more wealthy? We'll see how that works as we talk about other activities.

Trade

Perhaps the most fundamental economic transaction is a trade. I give you one or more assets that you want in exchange for one or more assets that you have that I want. There is a change of ownership and that's pretty much all there is to it. To be considered fair, a trade must be equitable for both parties and ideally results in an increase in wealth for both parties. How is this ever possible? It occurs because the personal value of assets differs between the participants in the trade. If I have more of some asset than I can ever possibly use and my neighbor has more of some other asset than he can possibly use, then trading some of my excess for some of his can result in an overall increase in wealth for both of us.

It is in the context of trade that the classical laws of supply and demand arise. If something that we want is readily available, then we would typically not want to trade much of our existing assets to get it. But when an asset is rare and the number of persons who desire it is much greater than the supply, the owner of that asset can demand much more in any trade for it. Note that if absolutely all buyers shared exactly the same value, then it would never be possible to charge more than that value and it would never be necessary to charge less than that value in order to sell one to each potential buyer. The classical law of supply and demand generally holds that there is a curve that defines how much of some product producers are willing to supply at each price point (which goes up as the price increases) and another curve that defines how much of a product consumers are willing to purchase at each price point (which goes down as the price goes up). Where the two curves intersect defines both the ultimate price of the product and how much is available for sale in an open market. Note that this depends crucially on there being a range of values held by potential buyers and also by potential suppliers.

Scarcity can be a local phenomenon. Something that is easily acquired in one location may be very rare in another. This observation leads to trading activities that seek to acquire a product where it is common and transport it to another locale where it is rare and can be traded again for assets of great value. History is replete with examples of this activity: the silk road between China and Europe, the spice trade of the far East, fur trading in North American, and many many more. Today, in our increasingly global economy, large companies take advantage of the relative differences in asset values around the world to increase the productivity and profitability of their economic transactions. They trade for (acquire) labor where it is cheap and use it to produce products that are sold (i.e. traded for money) where they are more highly valued.

Scarcity may also be created intentionally. A monopoly can be created by acquiring most or all of one type of asset and then trading it a little at a time over a long period. As the supply is made very small at any given time, the relative value of the asset to those who desire it will go up. Some monopolistic practices in some economic societies are now considered to be a form of unfair trade and subject to regulatory sanctions. Others are considered to be useful. For example, a government-issued patent essentially grants a monopoly on some technology asset for a number of years. That is usually a good thing because it promotes the development of new technology. It is more valuable to the developer because the monopoly makes it possible to sell or license the technology for more money.

Trading can carry the risk of failure. If the assets acquired cannot in turn be exchanged for as much as anticipated, then the profit margin associated with a trade drops and may even be negative, meaning that the trader ends up with assets of lower value than those they originally possessed. For example, prior to the 2008 economic recession there was a increase in the value of stocks as investors anticipated that they would be able to trade those stocks at some future time to increase their personal assets. But as we all know, those stock values dropped precipitously, turning such trades into losing propositions (at least until the stock value rose back up to the level it had when it was obtained).

Manufacture

Manufacturing is a process that transforms one set of assets into another set with higher value. Typically it involves the application of time in the form of labor and technology to transform commodities and property into other properties. As with most economic activity, the general goal of such a transformation is to produce property with more value. Input assets are often referred to by accountants and economists as the cost of goods, and output assets are usually called products. Manufacturing is almost always coupled with trading activity. The manufacturer trades the produced products for something of greater value. The increase in asset value that is realized by the company after trading the results of the manufacturing process is referred to as its profit. If the resulting net value of assets is less than the value of the assets used, then the process resulted in a loss rather than a profit.

What happens if the demand for some product suddenly decreases? In some cases it may be possible for a manufacturer to withdraw it from the market and wait for the demand to increase again. But usually there are costs associated with this delay that effectively eat up the profit of the manufacturing process over time. As you will understand later when I talk about investment activities, holding onto a product in anticipation of it having a greater value later is effectively investing in that product. Investments have their own forms of productivity and risk associated with them.

I must say something here about the role of technology in improving manufacturing productivity. Any tool improves productivity to the extent that it lets a person do more of some task or do it with higher quality or more precision or do it faster or do something that isn't even possible at all without the technology. Technology is a broad category that includes more and more sophisticated tools. The high degree of wealth that we have as a society today is in large part directly attributable to the high productivity that is possible using sophisticated modern technology. And we've only just begun ...

Develop

Development is an economic activity that is similar to manufacturing in that it transforms assets into other assets of more value using labor and technology. The subtle difference here is that the asset that results is typically some enhanced version of one of the input assets. An example will make this clear. We can talk about developing a property by adding a road that leads into it, clearing away debris, adding sewer and water, etc. The resulting property is fundamentally the same property, but it now has a greater value than it did before the development.

Sometimes developing part of an asset may make the rest of it more valuable. Real estate can be made more valuable by developing a small part in the middle. If, for example, a business is put there that is guaranteed to draw many customers into the area, then the value of the surrounding real estate will go up considerably.

The risk associated with development is that the anticipated increase in value to some other party may not materialize.

Market

Marketing is an interesting subject. It increases wealth not by changing an asset in any real way, but rather by changing the perception of the value of that asset in the minds of potential trading partners. In effect it increases the desirability or cachet of an asset. It may also simply increase awareness of the product, thus increasing the number of potential trading partners. The consequent increase in demand makes trades more profitable.

There is, of course, a whole literature associated with how to market so I won't try to summarize it here. Suffice it to say that almost all marketing is intended to increase the perceived value of the assets that some economic entity is offering for sale.

There are risks inherit in marketing of course. The expected increase in cachet may be subject to the whims of fashion. And of course products often compete and the marketing of a competitor may offset or completely negate the marketing done for a product. But if we can judge by the amount of money spent in the U.S. for marketing, it must be a very profitable economic activity.

Learn / Research

Learning is an economic activity? Absolutely! Learning is the process of exchanging time for knowledge and/or skill. Increasing those assets makes it possible to combine them with our time and engage in labor that is valued more highly by employers. Engaging in the learning activity begins at birth and is one reason why we must consider all children as economic persons. The more they learn during a given period of time, the more productive that learning is.

Not all learning increases the value of one's labor of course. Children who learn anti-social behaviors may find themselves at a serious competitive disadvantage in the labor market. The other risks associated with learning are that the knowledge learned may turn out to be less in demand in the future or may be so common that the perceived value is less.

Typically when we talk about research we think of scientists laboring in their laboratories. But research occurs in many forms. Every time someone invents a new way to do something more efficiently, it is the result of research. I think of research as directed learning. That is, learning that is devoted to finding answers to specific questions or solutions to specific problems. Better technology is the driver of increased productivity, but research is what drives both the development of new technology as well as new types of products that will be desired by the society. Although there are other drivers of overall societal wealth, research is right up there with the most significant ones.

Is there a risk associated with research? Definitely. As technology becomes more sophisticated, the assets needed to conduct research become increasingly more expensive to acquire. In a nutshell, it just costs a lot to do bleeding edge research. And the likelihood that the research will hit a dead end or result in no immediately available new technology or products can be significant. Over my lifetime I have witnessed a definite diminishment of research done by private companies. Even so-called applied research is now relegated to Universities. And the abstract / pure research that Universities used to do exclusively has diminished. Large companies now find it more economical to wait for some startup company to produce a new technology or prototype product and then acquire that startup than to do their own research. If one out of ten startups actually succeeds, then large companies can save substantial amounts of money in this fashion. Of course there is a risk that a competitor will acquire the startup first or that it will be so successful that the price of such an acquisition is prohibitive. So there are many risks no matter which path is taken.

Invest

I should say at the start of this discussion that the term investment can mean different things. To an economist, investment is any purchase of capital equipment that will be used as part of the subsequent manufacture or production of goods that will then be sold. This is NOT the sense in which I use the term here and hopefully the reader will not be confused.

Investment, as the term is used here, refers to an economic activity where an asset is acquired and held for some time in the expectation that it will be worth more at a later time. Some investments are relatively safe and some are quite risky. Generally speaking if a risky investment succeeds, the expectation is that it will have a substantially higher value in the future than that of a safe investment that succeeds. This is the sense in which a typical individual invests in the stock market. They purchase stocks in the expectation that they will increase in value over time. Note that economists do NOT consider this to be investment. Rather, they consider this to be a form of saving.

Does the notion of profit margin apply to investments? Yes, but we need to take into consideration the time factor. Just intuitively if two investments result in the same increase in wealth, but one does so over a short period of time and the other over a much longer period, then the first one could be characterized as more profitable. If the second one takes twice as long, then we could make two investments similar to the first one and increase our wealth by twice as much as the second investment. So the time for an investment to mature is very important.

We previously characterized profit margin as the ratio between the value of profit to the value of output assets: Vp / Vo. We can easily modify this to account for time to: Vp / (Vo * T) where T is the time required to realize the gain. This definition can now be applied to the usage of any assets. That let's us ask questions that compare different forms of economic activity according to the time required to complete them. Doing many discrete activities that each occur very quickly but increase wealth only a little, may be a better use of our assets than doing a single activity that provides a substantial increase in wealth, but takes a very long time to complete. As individuals we make this sort of intuitive judgment all the time. Do I take a job that pays a little every day or do I start a company and work for potentially a very long time for little or no compensation in order to increase my wealth more dramatically later on? Obviously the risk associated with the various activities also plays a role in such assessments.

Some types of investment can take years to provide a substantial addition to wealth. Some new types of investment are completed in milliseconds. There are new automated stock trading programs that can decide to make an investment and then sell it off in anywhere from fractions of a second to several minutes. This is a new sort of investment that I'll have more to say about later.

Gambling can be characterized as an extremely risky investment. Arguably, some of the investments that Wall Street firms made in mortgage-backed securities prior to the great recession of 2008 were tantamount to gambling as was the sale of some derivatives. But perhaps that is a topic for another paper ...

Assets acquired by investment may also have ongoing expenses associated with them that effectively diminish the profitability of the investment. For example, a parcel of real-estate might be acquired in the anticipation that new development in its vicinity will eventually make it worth much more that its original value. But the investor likely has to pay property taxes on the parcel while waiting for the value to reach a value considered reasonable. There is also something called the time cost of money. The idea here is that an asset that is not being used to produce new wealth in a reasonable amount of time is being wasted or at least used in a less profitable fashion that it might be.

Rent / Lease

These economic activities create wealth by taking advantage of a relatively short-term need for the use of some asset. If an asset can be acquired and then effectively time-shared among multiple persons who need the use of it at different times, then wealth can be created. Perhaps the prototypical example of this is automobile rentals. A person who needs a car in a particular place for a small number of days or weeks will be willing to exchange some amount of assets to satisfy that need. If that amount is more than the pro-rated value of the car for that period of time, then the wealth of the car owner can be increased by making that trade. The value equation for a lessor is more complicated than that of course, but you get the idea.

The risk of this activity is that there will be no demand for the assets that were acquired with the intent of renting them out. An idle asset is a wasted opportunity.

Loan / Provide Credit

Loans are economic activities undertaken by banks and other financial organizations. There are two fairly different ways to do this. One way is done by banks with specific charters from the government that permit them to create money right out of thin air and then lend it to you. When you pay it back with interest, the banks keep the interest as income and the principle amount of the loan disappears back into the ether that it came from. Many, perhaps most, people are under the impression that banks loan out the money that people deposit with them in checking and savings accounts, and although that is essentially a correct model for credit unions and money market deposits, it is incorrect for chartered banks. But that is the second method of making loans.

Let's start with a discussion of how chartered banks loan money that they create themselves. In return for allowing banks to create money in this way, the government imposes regulations that require banks to have a sufficient amount of capitalization (i.e. either money that came to the bank from those who invested in its stock or retained earnings from previous operations). A ratio between capitalization and the amount of outstanding loans must be maintained to assure that the bank can always back up the demand for the funds that it makes available via loans even if some of the borrowers themselves default and never pay back their loans.

Understanding these capital requirements is key to understanding how banks sometimes fail. You may have heard or read about "toxic assets" that the Federal Reserve purchased from large banks as part of their effort to keep banks solvent. What happened is that the banks were holding as part of their capital a large number of financial assets that ultimately depended on a whole host of sub-prime mortgages being paid back. Those assets were assigned a value that was consistent with the assumption that they WOULD be paid back. When the housing bubble collapsed, all of a sudden those assets became MUCH less valuable than they were previously assumed to be. This was an unexpected systemic failure. If the banks restated their capital holdings in terms of the new market value of those assets, then their capital to loan ratios would have fallen below the level required and they would have had to either acquire more capital from somewhere or call in lots of loans. The U.S. government helped them in multiple ways at different points in time. They recapitalized them by essentially loaning them money that counted towards their capital requirements and also purchased many of those mortgage-related financial assets at their face value rather than a their market value so that the U.S. government absorbed the losses rather than making the bank do so. It's rather interesting to discuss whether this is ultimately what the government should have done, but it clearly avoided a domino effect avalanche of bank failures.

Banks in the U.S. are also required to maintain reserves in proportion to the amount of loans outstanding. Reserve funds consist of money that is on deposit with the Federal Reserve bank or cash kept in the bank's vault. The primary use of reserves is to clear transactions between banks. When you write a check to someone else and they deposit it, the check clears when your bank transfers reserves in that amount from its Fed account to the account of the bank where the check was deposited. You may see a description in some economic texts which will tell you that the amount that a bank can loan is restricted by the amount of reserves (according to the fractional reserve formula), but in a very practical sense this is not how it works. A bank will first make a loan and then if it needs to acquire additional reserves in order to satisfy the reserve requirement for the amount of its outstanding loans, it will get those reserves by borrowing them either from other banks or the from the Federal Reserve itself. Understanding this process would require a longer explanation that will have to wait for another time.

So let's go back and think about these sorts of loans as economic activities that create wealth. What exactly are the inputs to this process since we said that the money which is loaned is created from nothing? In a real sense the capital of the bank is part of the input. It's not that the capital itself is being loaned out, but rather that the requirement that banks maintain a specified capital ratio means that there are limits to how much they can loan. Loans that are paid back at high interest are obviously more profitable than those which are paid back at lower interest or not paid back at all.

Earlier I said that money-market funds and credit unions create loans in a different fashion. They do actually use money as input. They take deposits and pay some rate of interest, but then make it available to a borrower in exchange for a larger amount of money returned over time, typically in periodic payments. Lending differs from investing because there is typically no presumption that the asset will appreciate over time. Rather the lender gets back the original asset plus interest payments. Note that money-market funds clearly cannot lend out all their deposits or they would be unable to accommodate withdrawals. While money-market funds and credit-unions have come to be considered essentially risk-free they do, in fact, pose some risk to depositors. It is possible that they could lose all money deposited with them if a series of very bad loans left them insolvent.

Providing credit is a similar activity. An arrangement is made such that a borrower can instantly get a loan of up to some previously arranged limit for some purpose. Credit cards are one form of this that most of us are familiar with. When we use a credit card to purchase something the card company grants us an instant loan that is used to pay the vendor of the purchased item. Most of us find this a nice convenience and shop in places that accept our cards which makes it possible for the credit card company to charge a fee to vendors for the privilege of accepting their card. In addition, they are happy to extend the term of our loan in exchange for interest and other fees.

I have barely scratched the surface of what could and should be said about money. I will leave that for a bit later.

Consume

Consumption is an activity that takes an EVA as input and removes it from the economy. In some sense it is exchanged for some IVA. The obvious example is the consumption of food and most consumer products. They are bought and used for a period of time and either disappear or depreciate to nothing of value. These activities are profitable for the person who does them because they derive some type of IVA from them. They are hopefully healthier or happier because they have consumed.

Ultimately consumption drives every other economic activity. When the rate of consumption is high the economy will be booming and when the rate of consumption is very low, it will often enter a recession or depression. Consumption drives the creation of goods and services, results in job creation, and generally motivates all beneficial economic activity.

There are risks to consumption, just as there are risks to every other type of economic activity. The IVAs gained may turn out to have less value than anticipated resulting in a net loss of assets that is regretful. The long-term risks are to society as a whole. If we consume irreplaceable resources then we may impoverish future generations and perhaps pose a risk to their very existence.

Combining Economic Activities

Almost every economic organization will combine two or more of the activities just described and most will engage in many of them. Experienced corporate managers understand the best way to combine them to maximize the creation of new wealth.

II.F. Government Economic Activity

Governments are special types of organizations that deserve some additional discussion. In addition to undertaking economic actions as other persons do, they can engage in special sorts of economic transactions. They can create the regulations that govern other economic activities within their jurisdiction and they can impose taxes within that jurisdiction.

Regulations are created by governments to assure that economic activities are orderly. Typically their objective to to make these transactions as fair as possible for all parties. Assuring fairness is especially important for transactions between large and powerful organizations and individuals or when one party has access to information that the other does not. They also make economic activity more efficient because they make it unnecessary for the participating persons to renegotiate the terms of each and every transaction. Regulations can also provide protection to persons in the form of legal remedies if regulations are violated by one of the parties in some way. Regulations impose obligations and consequent cost on persons and also costs on the government that must oversee and enforce them. Because of this, regulations can be the subject of intense debate when viewed as especially onerous, costly, or unfair.

The government of the United States creates regulations for international and interstate commerce by provision of Article I, Section 8 of the U.S. Constitution which among other things grants to congress the right: "To regulate Commerce with foreign Nations, and among the several States, and with the Indian Tribes;". Each state has the right to regulate commerce within itself. Much of the lobbying that goes on in Washington is associated with influencing the creation and enforcement of regulations.

Governments can exist at many levels of course, so each economic action may be governed by the regulations of several different governments. We'll look more closely at the nature of all economic activities undertaken by governments a bit later.

Economic Model and Terminology

11/9/11